Robinhood is undercutting the big banks by forgoing brick-and-mortar branches with its new zero-fee checking and savings account features. With no overdraft or monthly fees, a juicy 3 percent interest rate, and a claim of more US ATMs than the five biggest banks combined, Robinhood is using the scalability of software to pass impressive perks on to customers. The free stock trading app already used that approach to attack brokers like E*Trade and Charles Schwab that charge a per trade fee. Now it’s breaking into the larger financial services market with a model that could put the squeeze on Wells Fargo, Chase, and Bank Of America.

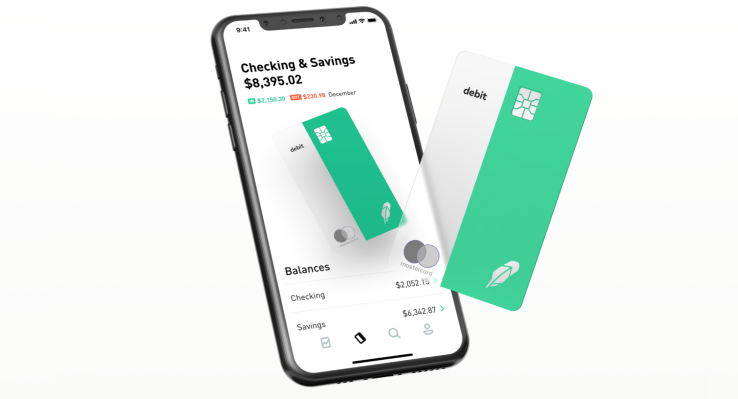

Today Robinhood launches checking and savings accounts in the US with a Mastercard debit card issued through Sutton Bank that starts shipping December 18th. Users earn 3 percent on all the dough they keep with Robinhood, yet there’s no minimum balance or fees for monthly membership, overdrafts, foreign transactions, or card replacements. That’s a pretty sweet deal compared to the other leading banks that all charge for some of that or offer much lower interest rates. The tradeoff is that while customers get 24/7 live text chat support, they won’t be able to walk into a local bank branch. Users who want early access can sign up here.

Robinhood expects to turn a profit thanks to a lean 300-employee operation, earning a margin on investing your money in US treasuries, and a revenue share with Mastercard on interchange fees charged to merchants when you swipe. The launch could be critical to keeping Robinhood worthy of its $5.6 billion valuation from when it took a $363 million Series D in March just a year after raising at a $1.3 billion valuation. The 6 million-user app invested in launching a free cryptocurrency trading exchange early this year only to see coin prices plummet and mainstream interest fall off. But with banks hammering users with surprise fees and mediocre user experience, there’s a huge opportunity for a mobile-first startup to disrupt how we store money.

“Brick-and-mortar locations are costly. Our goal with this product was to build a completely digital experience so we can reduce our overhead so we can pass more of the value back to customers” Robinhood co-CEO Baiju Bhatt tells me. [Disclosure: I know Bhatt and co-CEO Vlad Tenev from college] “Saving accounts in the US pay on average 0.09 percent and we all know the banks are making far more than that from the deposits. With Robinhood you earn 3 percent off all of your money. Mental math is hard so if you look at the median US household that has about $8000 in liquid savings, they’d earn $240 a year.”

Robinhood will be sending invites to users in January for the new feature that they can use exclusively or alongside their existing bank. Anyone approved to use Robinhood’s stock brokerage is eligible, but users can also sign up directly for checking and savings with no obligation to trade stocks. Robinhood claims signing up won’t impact your credit score. Users get to customize a Robinhood-branded debit card that’s accepted wherever Mastercard is. Since the feature is run within Robinhood’s brokerage, it’s ensured by the SIPC instead of the FDIC, but you still get the same insurance on up to $250,000 cash.

One of the most appealing features of Robinhood checking and savings is getting access to 75,000 free-to-use ATMs in places like Target, Walgreens, and 7-Eleven. Users won’t be able to tell just by looking at an ATM whether it’s in the network, but the Robinhood app features a map for finding the nearest one. You can deposit checks via Robinhood’s app too, and if you need to send a check, you can just tell the startup how much to deliver to whom and it will mail the check for you.

“These fees like overdraft fees — they’re not fees millionaires are paying. It’s ordinary folks paying. It’s actually more expensive for those that have less money and it’s cheaper for those that have more money. We think that isn’t right and we think that’s bad business” Bhatt gripes. Because Robinhood built its own clearing house for moving money, and it lacks the overhead of traditional banks, it’s able to save enough money to make its no-fee structure work. “We want to build a financial services company that democratizes America’s financial system.”

Robinhood will have to convince users it’s worthy of their trust, as a security breach could be disastrous. There’s also the question of whether people are ready to ditch their bank branch. “Behaviors about and going into a branch are definitely changing” says Bhatt. My biggest concern was not having any consistency in who I talk to when I need banking help. Bhatt tells me the company plans to roll out more personalized customer service features in the coming months, but there may always be edge cases that make the lack of in-person support annoying.

Getting into banking could open a lucrative revenue stream for Robinhood as it charts its path to IPO. The startup recently hired Jason Warnick, a 20-year veteran of Amazon, to be its CFO and get it prepped to go public. Wall Street will want to see a more robust business that’s not as vulnerable to foes like stock brokerage Charles Schwab which is already lowering fees to stay competitive with Robinhood. Not only will checking and savings see users move more money into their Robinhood accounts that it can invest to earn a profit, but it also poises the startup to tackle more financial services in the future.

Be the first to comment